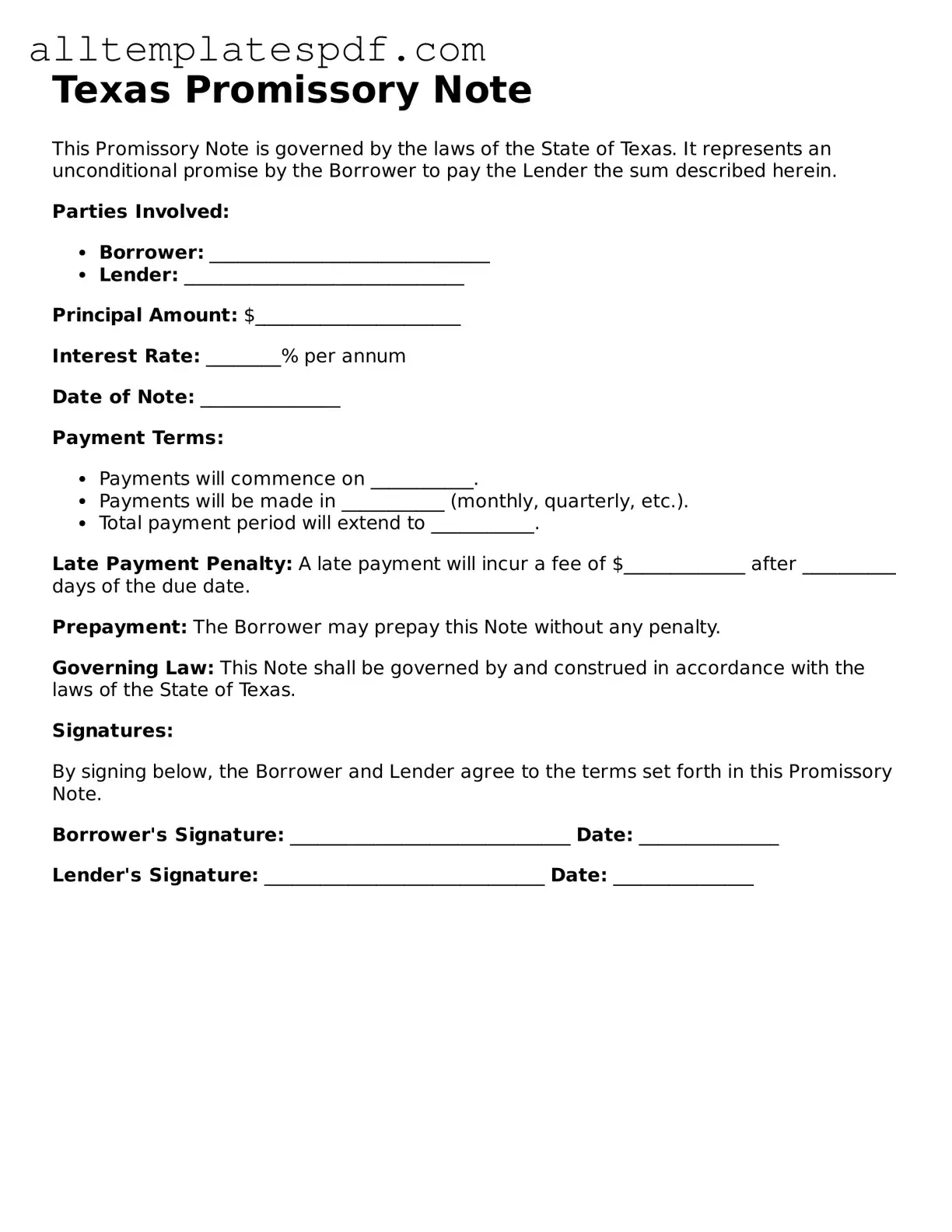

Blank Promissory Note Template for the State of Texas

Blank Promissory Note Template for the State of Texas

Filling out the Texas Promissory Note form can be a straightforward process, but many individuals make common mistakes that can lead to complications. Understanding these pitfalls can help ensure that the document is completed accurately.

One frequent error is failing to include all necessary parties. It is essential to list both the borrower and the lender clearly. Omitting a party can create confusion and complicate the enforcement of the note.

Another mistake is not specifying the loan amount. The total amount borrowed should be clearly stated to avoid disputes later. Ambiguities regarding the amount can lead to misunderstandings between the parties involved.

Many people also overlook the interest rate. If the note includes interest, the rate must be clearly defined. A vague or missing interest rate can result in legal challenges and financial discrepancies.

Additionally, incomplete payment terms are a common issue. The schedule for repayments, including due dates and amounts, should be explicitly outlined. Without this information, it may be difficult to enforce the terms of the agreement.

Another area of concern is neglecting to date the document. A date is crucial for establishing the timeline of the agreement. Without it, there may be confusion regarding when the loan was initiated.

Some individuals fail to sign the document. It is vital for all parties to sign the promissory note to validate the agreement. A missing signature can render the document unenforceable.

Moreover, not having a witness or notarization can be problematic. While not always required, having a witness or notarizing the document adds an extra layer of authenticity and can help prevent future disputes.

Another common mistake is using unclear language. It is important to use straightforward language to avoid ambiguity. Legal terms or overly complex wording can lead to misunderstandings and complications.

Lastly, failing to keep copies of the signed document is a mistake that can have serious consequences. Each party should retain a copy for their records to ensure that everyone has access to the agreed-upon terms.

By being aware of these common mistakes, individuals can fill out the Texas Promissory Note form more effectively, reducing the likelihood of future issues and ensuring a smoother lending process.

Promissory Note Template Georgia - The borrower must provide accurate information to ensure the validity of the note.

The New York 810 form is an official document used typically by law enforcement agencies to report certain types of incidents. It's a critical component of the administrative process that ensures incidents are recorded accurately and consistently. For those looking to access the form, resources such as NY PDF Forms provide a streamlined approach for documentation, serving as a vital record for future reference and accountability.

Simple Promissory Note Template California - A promissory note can often be transferred or sold to another party, depending on terms.

Michigan Promissory Note Example - A promissory note is a straightforward way to formalize a loan agreement.

Online Promissory Note - This form can simplify the process of borrowing and lending money.

There are several misconceptions about the Texas Promissory Note form. Understanding these can help clarify its purpose and usage.

This is not accurate. A promissory note is a written promise to pay a specific amount of money. A loan agreement, on the other hand, includes terms and conditions related to the loan, such as interest rates and repayment schedules.

This is not required in Texas. While notarization can add an extra layer of authenticity, it is not a legal requirement for the note to be enforceable.

Individuals and businesses can also create promissory notes. Anyone can issue a note as long as they are lending money and both parties agree to the terms.

This is misleading. While some notes may not include a detailed repayment schedule, having one can help clarify expectations and avoid disputes between the parties involved.

| Fact Name | Description |

|---|---|

| Definition | A Texas Promissory Note is a written promise to pay a specified amount of money to a designated person or entity at a defined future date. |

| Governing Law | The Texas Promissory Note is governed by the Texas Business and Commerce Code, specifically Chapter 3. |

| Parties Involved | The note involves two primary parties: the borrower (maker) and the lender (payee). |

| Payment Terms | The note must clearly outline the payment terms, including the principal amount, interest rate, and payment schedule. |

| Interest Rate | Texas law allows for both fixed and variable interest rates, but the rate must be stated in the note. |

| Default Clause | A default clause is often included, detailing the consequences if the borrower fails to make payments. |

| Signatures | The note must be signed by the borrower to be legally binding. |

| Notarization | While notarization is not required, it can provide additional legal protection for the lender. |

| Transferability | Texas Promissory Notes can be transferred or assigned to another party, allowing for flexibility in financing. |

Once you have the Texas Promissory Note form in hand, it's essential to complete it accurately to ensure that all parties involved understand their rights and obligations. This document will serve as a legal record of the loan agreement, outlining the terms clearly. Follow these steps to fill out the form correctly.

After completing the form, ensure that both parties retain a copy for their records. It is advisable to consult with a legal professional to review the document before finalizing the agreement. This step can help prevent misunderstandings and protect the interests of both parties.