Attorney-Approved Promissory Note for a Car Template

Attorney-Approved Promissory Note for a Car Template

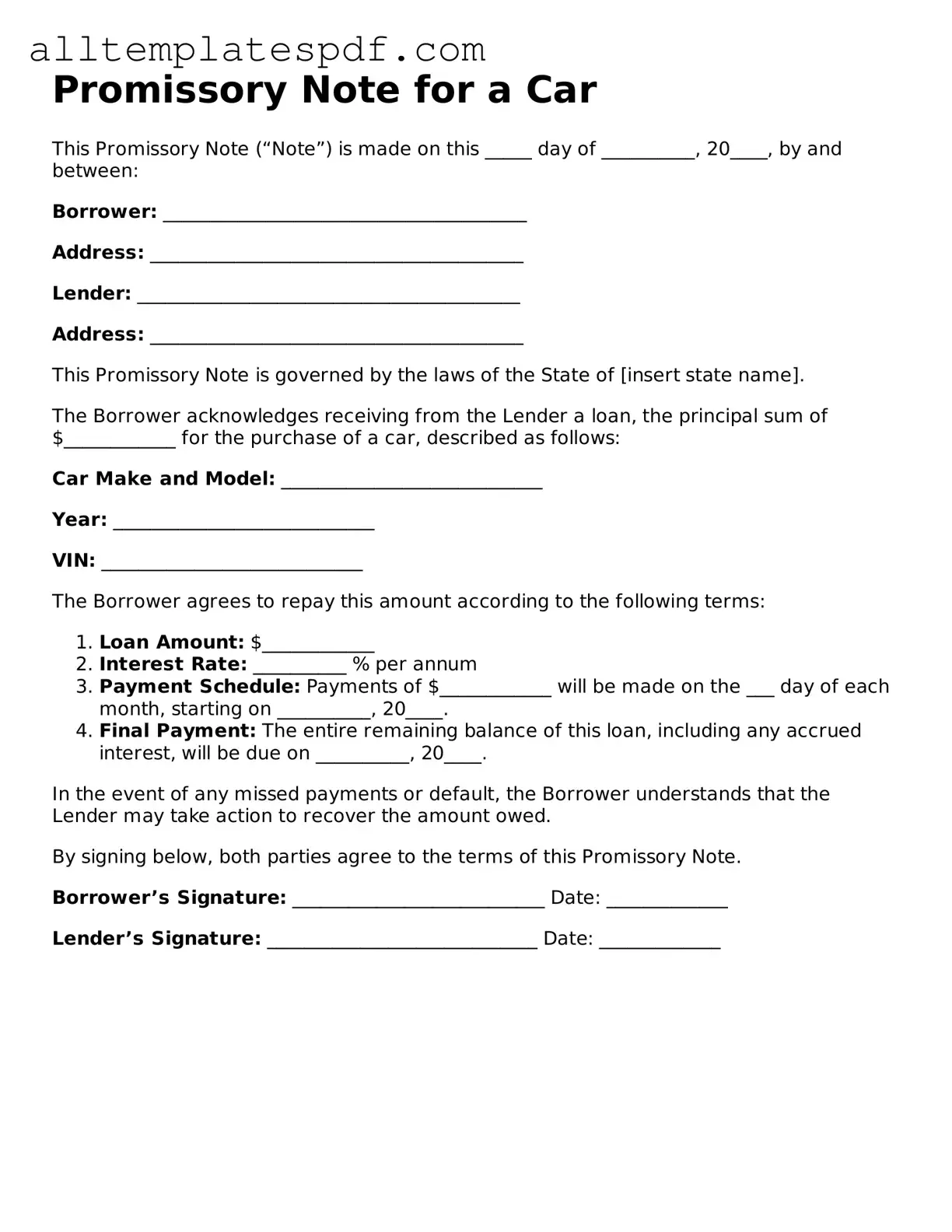

When filling out the Promissory Note for a Car form, individuals often overlook important details that can lead to complications later on. One common mistake is failing to include all necessary information about the borrower and the lender. Both parties' names, addresses, and contact information must be clearly stated. Omitting any of these details can create confusion and hinder communication, especially if issues arise regarding payment.

Another frequent error involves not specifying the loan amount accurately. Borrowers sometimes write down an incorrect figure or forget to include additional costs such as taxes or fees. This can result in misunderstandings about the total amount owed. It is crucial to ensure that the loan amount reflects the precise cost of the vehicle, including any agreed-upon interest rates.

Many individuals also neglect to outline the payment terms clearly. This includes the payment schedule, interest rate, and any late fees. Without clear terms, both parties may have different expectations, leading to disputes. It is advisable to be explicit about when payments are due and how they should be made to avoid future complications.

Additionally, failing to sign and date the document is a common oversight. A Promissory Note is not legally binding unless it is signed by both the borrower and the lender. Some individuals may forget this step, thinking that verbal agreements or informal arrangements are sufficient. Without signatures, the note may be deemed invalid, leaving both parties unprotected.

Lastly, individuals sometimes do not keep copies of the signed Promissory Note. It is essential to retain a copy for personal records. This serves as proof of the agreement and can be invaluable in case of disputes or misunderstandings. Keeping a well-organized file of all related documents can provide clarity and reassurance for both parties involved in the transaction.

Promissory Note Paid in Full Template - A valuable resource for both parties in a lending agreement.

In Florida, utilizing a well-structured Promissory Note is vital for securing loans and ensuring both parties are aligned on repayment expectations; resources like Florida Forms can provide essential templates and guidance for drafting this important document.

When it comes to the Promissory Note for a Car form, several misconceptions often arise. Understanding these can help individuals navigate the process more effectively.

This is not true. A promissory note is a legal document that outlines a borrower's promise to repay a loan. The car title, on the other hand, is proof of ownership of the vehicle.

Simply having a promissory note does not guarantee that a loan will be approved. Lenders consider various factors, including creditworthiness and income, before making a decision.

This is incorrect. Borrowers can negotiate the terms of a promissory note, such as the interest rate and repayment schedule, before signing it.

While it is not always necessary, having a witness or notary can add an extra layer of security and validity to the document. Some lenders may require this as part of their process.

| Fact Name | Description |

|---|---|

| Definition | A promissory note for a car is a written promise to pay a specific amount of money for the purchase of a vehicle. |

| Parties Involved | The document typically involves two parties: the borrower (buyer) and the lender (seller or financing institution). |

| Governing Law | The governing law can vary by state; for example, in California, the Uniform Commercial Code (UCC) applies. |

| Payment Terms | It outlines the payment terms, including the total amount financed, interest rate, and repayment schedule. |

| Default Clause | The note often includes a default clause, which details the consequences if the borrower fails to make payments. |

| Secured vs. Unsecured | Typically, a promissory note for a car is secured by the vehicle itself, meaning the lender can reclaim the car if payments are not made. |

| Transferability | These notes can often be transferred to another party, allowing lenders to sell the debt to a third party. |

| Legal Enforceability | As a legal document, it is enforceable in court, meaning a lender can take legal action to recover owed amounts. |

| Signatures Required | Both the borrower and lender must sign the note for it to be valid and enforceable. |

| State-Specific Variations | Different states may have specific requirements or forms; for instance, Florida has unique regulations under its state laws. |

After gathering the necessary information, you can proceed to fill out the Promissory Note for a Car form. Ensure that all details are accurate and clearly written to avoid any misunderstandings in the future.

Once the form is completed, keep copies for both parties. This ensures that everyone has access to the agreed-upon terms and conditions.