Attorney-Approved Promissory Note Template

Attorney-Approved Promissory Note Template

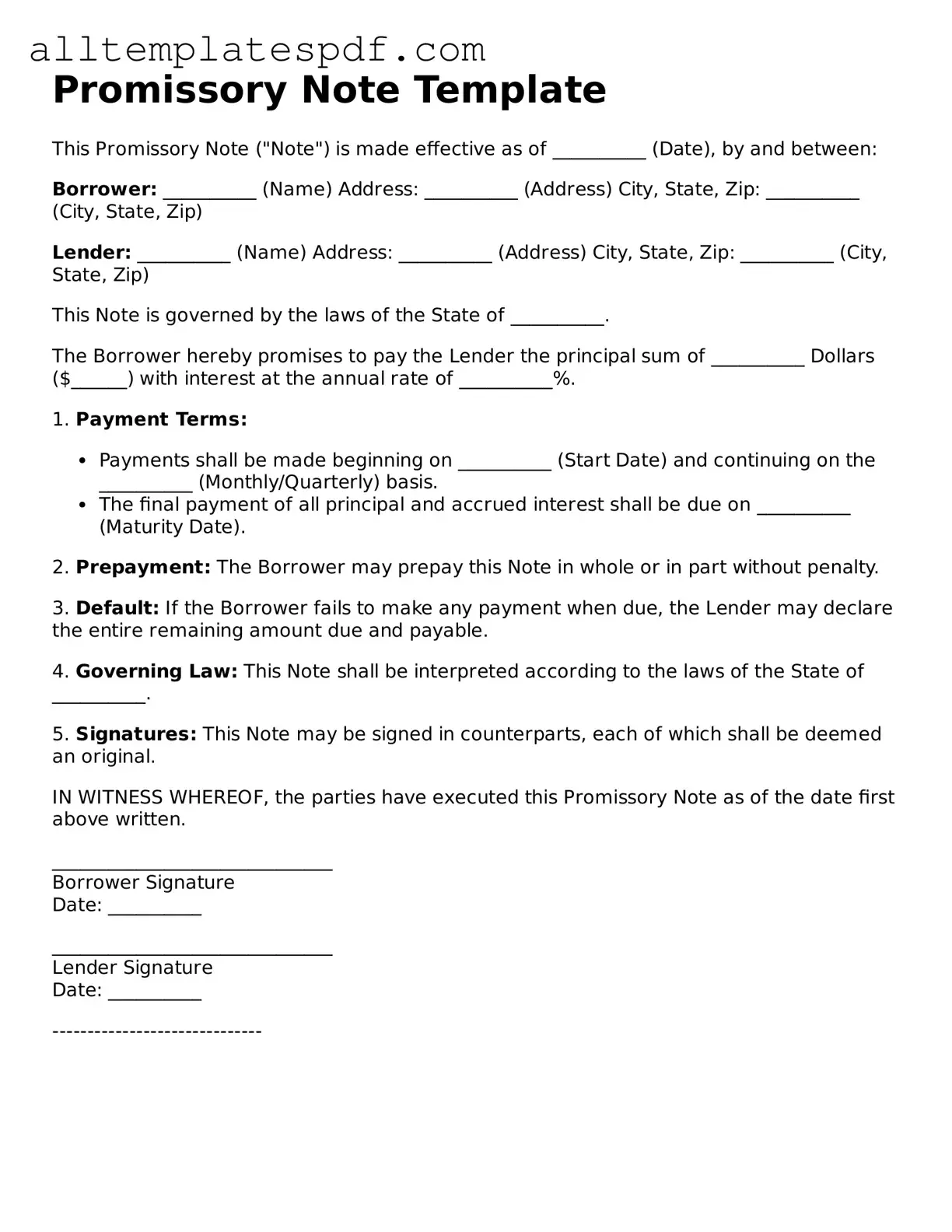

Filling out a Promissory Note can be a straightforward process, but several common mistakes can lead to complications down the line. One frequent error is failing to include all necessary details. A Promissory Note should clearly state the names of both the borrower and the lender. Omitting this crucial information can create confusion and may lead to disputes about the terms of the agreement.

Another mistake often made is neglecting to specify the interest rate. Without a defined interest rate, the terms of repayment become ambiguous. This can result in misunderstandings and potential legal issues. It is essential to clearly outline whether the loan is interest-free or what the applicable interest rate is, to avoid any future conflicts.

Many individuals also forget to include the repayment schedule. A Promissory Note should detail how and when payments will be made. This includes the frequency of payments—whether they are monthly, quarterly, or otherwise—and the due dates. Without this information, borrowers may struggle to meet their obligations, and lenders may face uncertainty regarding when they can expect repayment.

In addition, some people overlook the importance of signatures. Both parties must sign the Promissory Note for it to be legally binding. A missing signature can render the document unenforceable, leaving the lender without legal recourse if the borrower defaults on the loan.

Another common oversight is failing to indicate the consequences of default. A well-drafted Promissory Note should outline what will happen if the borrower fails to make payments as agreed. This could include late fees, acceleration of the loan, or other remedies. Without these provisions, lenders may find themselves with limited options should the borrower default.

Lastly, individuals sometimes neglect to keep a copy of the signed Promissory Note. It is vital for both parties to retain a copy of the document for their records. This ensures that both the lender and borrower have access to the agreed-upon terms, which can be critical in the event of a dispute. Keeping a copy helps protect the interests of both parties involved.

Artwork Release Form Template - This document should be retained for reference regarding the usage of artwork.

Panel Schedule - A guide for ensuring circuits are balanced across the panel.

The importance of the New York DOS 1710 form goes beyond merely fulfilling legal requirements; it is essential for foreign professional service limited liability companies seeking to establish credibility and transparency in the state. To ensure compliance with publication mandates and navigate the complexities of the application process effectively, entities often turn to resources like NY PDF Forms, which provide valuable templates and guidelines for their documentation needs.

Week to Week Lease Agreement - This document helps ensure that the rental experience meets both parties' expectations.

Understanding the Promissory Note form is essential for anyone involved in lending or borrowing money. However, several misconceptions can lead to confusion. Here are ten common misconceptions:

By clarifying these misconceptions, individuals can better understand the importance and functionality of the Promissory Note form in financial transactions.

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money to a designated person or entity at a specified time. |

| Key Elements | It typically includes the amount, interest rate, maturity date, and the signatures of the borrower and lender. |

| Governing Law | In the United States, promissory notes are governed by the Uniform Commercial Code (UCC), which varies by state. |

| Enforceability | A properly executed promissory note is legally enforceable in court, provided it meets the necessary legal requirements. |

| Types | There are various types of promissory notes, including secured and unsecured notes, each with different implications for the borrower and lender. |

Once you have the Promissory Note form in hand, you are ready to begin the process of filling it out. This form will require specific information from you, and accuracy is key. After completing the form, you will likely need to keep a copy for your records and provide the original to the other party involved in the agreement.