Attorney-Approved Owner Financing Contract Template

Attorney-Approved Owner Financing Contract Template

Filling out an Owner Financing Contract form can be a straightforward process, but several common mistakes can lead to complications. One frequent error is failing to provide complete information. When individuals leave out essential details, such as the property address or the names of the parties involved, it can create confusion later on. Ensuring that all fields are filled out accurately is crucial for a smooth transaction.

Another mistake often made is misunderstanding the terms of the financing agreement. Some people may not fully grasp the implications of interest rates, payment schedules, or the total amount financed. This lack of understanding can lead to unrealistic expectations or disputes down the line. Taking the time to review and comprehend each term is important for all parties involved.

Inaccurate calculations can also pose significant issues. Errors in calculating monthly payments or total interest can result in financial strain. It is advisable to double-check all figures and, if necessary, seek assistance from a financial advisor or use a calculator designed for such purposes.

Omitting signatures is another common oversight. All parties must sign the contract for it to be legally binding. If one party forgets to sign, the contract may be rendered invalid. It is beneficial to have a checklist to ensure that all required signatures are obtained before finalizing the document.

Another mistake involves neglecting to include contingencies. Failing to outline conditions that must be met for the agreement to remain valid can lead to misunderstandings later. Including contingencies can protect both the buyer and seller, ensuring that all parties are aware of their obligations.

Some individuals also overlook the importance of including a clear description of the property. A vague or incomplete description can lead to disputes about what is being financed. Providing a detailed description helps to clarify expectations and responsibilities for all parties.

Lastly, people often forget to review local laws and regulations regarding owner financing. Each state has specific rules that govern these transactions, and not adhering to them can create legal issues. Researching local laws ensures that the contract complies with all necessary regulations, protecting both the buyer and seller.

Purchase Agreement Addendum - The addendum should reference the original purchase agreement for clarity.

Understanding the intricacies of a real estate transaction is crucial, and one way to simplify this process is by utilizing resources such as the NY Templates, which offers a comprehensive New York Real Estate Purchase Agreement that details the expectations and responsibilities of both the buyer and seller.

Buyer's Agent Termination Letter Sample - This form can simplify the process of returning deposits and resolving related issues.

Owner financing can be a beneficial arrangement for both buyers and sellers, yet several misconceptions surround the Owner Financing Contract form. Understanding these misconceptions is essential for making informed decisions.

This is not true. While owner financing can be an option for buyers with credit challenges, it is also used by those who may simply prefer the flexibility it offers compared to traditional financing methods.

In most owner financing agreements, the buyer assumes responsibility for repairs and maintenance once the sale is finalized. However, the specifics can vary based on the contract terms.

Owner financing is legal in most states, but it is subject to regulations. Both parties should ensure compliance with local laws and regulations when drafting the contract.

Buyers can often refinance a property purchased through owner financing, provided they meet the lender's criteria. The original contract should clarify any restrictions on refinancing.

While some buyers and sellers choose to work directly with each other, hiring a real estate agent can still provide valuable guidance and expertise throughout the process.

Interest rates in owner financing agreements can vary widely. They may be higher, lower, or comparable to traditional loan rates, depending on the terms negotiated between the buyer and seller.

When properly executed, an owner financing contract is legally binding. Both parties should ensure that the agreement is documented clearly and signed to protect their interests.

Owner financing involves paperwork similar to traditional transactions. Both parties should be prepared to complete necessary documentation to ensure a smooth transfer of ownership.

| Fact Name | Description |

|---|---|

| Definition | An Owner Financing Contract is an agreement where the seller finances the purchase of the property for the buyer, allowing the buyer to make payments directly to the seller instead of obtaining a mortgage from a bank. |

| Benefits | This type of financing can simplify the buying process, especially for buyers who may have difficulty securing traditional financing. It can also provide sellers with a steady income stream. |

| Governing Law | The laws governing Owner Financing Contracts vary by state. For example, in California, the contract must comply with the California Civil Code, while in Texas, it is governed by the Texas Property Code. |

| Payment Terms | Typically, the contract will outline the purchase price, down payment, interest rate, and payment schedule. These details are crucial for both parties to understand their financial obligations. |

| Default Consequences | If the buyer fails to make payments as agreed, the seller may have the right to foreclose on the property, similar to a traditional mortgage agreement. |

| Legal Considerations | It’s important for both parties to consult legal professionals when drafting the contract to ensure that all terms are clear and comply with state laws, protecting their interests. |

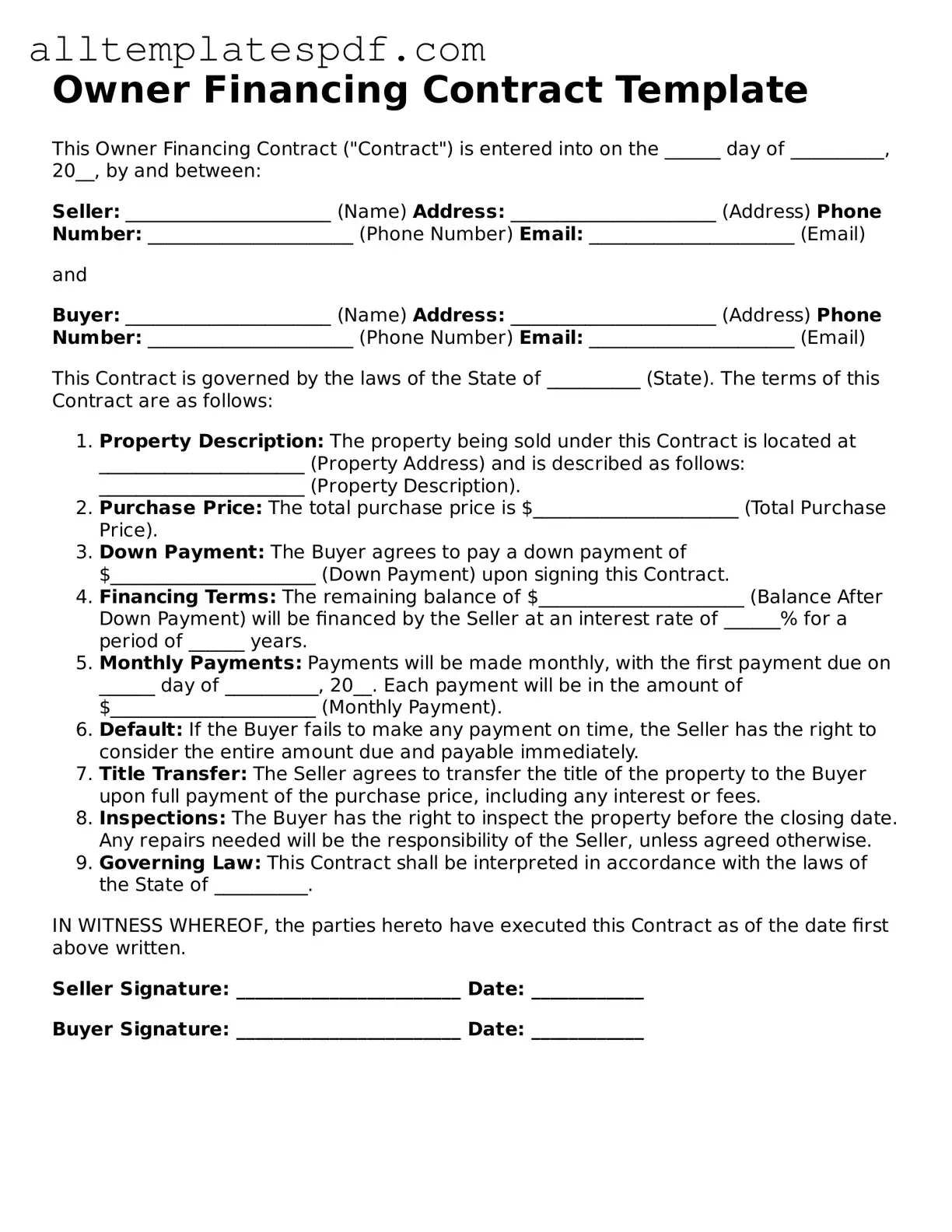

Filling out the Owner Financing Contract form is a crucial step in establishing the terms of a sale where the seller finances the purchase for the buyer. Completing this form accurately helps protect both parties and ensures clarity in the transaction. Follow these steps to fill out the form correctly.

After completing the form, review it carefully to ensure all information is accurate and complete. This attention to detail helps prevent misunderstandings and protects both parties involved in the transaction.