Blank Promissory Note Template for the State of New York

Blank Promissory Note Template for the State of New York

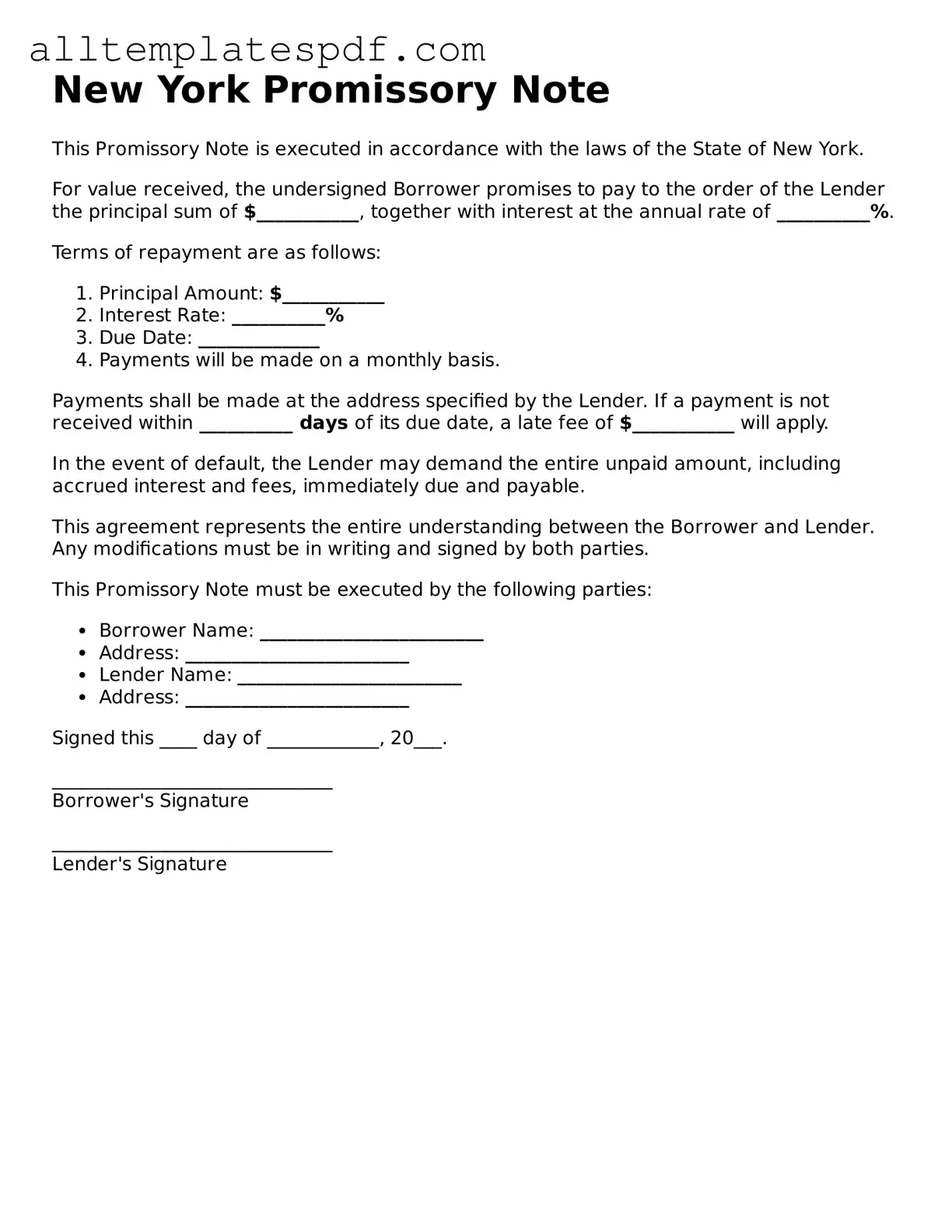

Filling out a New York Promissory Note form can be straightforward, but many individuals make common mistakes that can lead to complications. One frequent error is neglecting to include the date. The date signifies when the agreement takes effect and is crucial for establishing timelines related to repayment.

Another common mistake is failing to clearly state the amount being borrowed. Ambiguities in the loan amount can lead to disputes later on. It is essential to write the amount both in numbers and in words to eliminate any confusion.

People often overlook the importance of specifying the interest rate. Without this detail, the note may be considered unenforceable. If an interest rate is applicable, it should be clearly articulated to avoid misunderstandings.

Some individuals mistakenly forget to include the repayment terms. This section should outline how and when payments will be made. Without clear repayment terms, the borrower may struggle to understand their obligations.

Another mistake is not identifying the parties involved correctly. It is vital to include the full legal names of both the lender and the borrower. Inaccurate names can complicate enforcement of the note.

Additionally, many people neglect to sign the document. A signature is a critical component that indicates agreement to the terms laid out in the note. Without it, the document may lack legal validity.

Another oversight involves not providing a witness or notarization when required. While not always necessary, having a witness or notarization can strengthen the enforceability of the note.

Some individuals fail to keep copies of the signed note. Retaining a copy is important for both parties to refer back to the agreement and ensure compliance with its terms.

Lastly, people sometimes do not seek legal advice when drafting the note. While it may seem simple, consulting with a legal expert can help ensure that the document meets all legal requirements and adequately protects both parties' interests.

Michigan Promissory Note Example - This note is often used in real estate transactions for buyer financing.

For those looking to obtain marriage records from the City of New York, understanding the New York CC2002B form is crucial, and resources such as NY PDF Forms can provide the necessary guidance to navigate this process effectively. Applicants are required to meet specific conditions for record access, ensuring that the details submitted are accurate and legally compliant.

Online Promissory Note - This form formalizes a loan agreement between the lender and the borrower.

Understanding the New York Promissory Note form can be challenging due to various misconceptions. Here are ten common misunderstandings that people may have:

While many promissory notes share basic elements, each state has its own requirements. The New York Promissory Note form has specific rules and language that must be adhered to.

Although verbal agreements can sometimes be enforceable, a written promissory note is essential for clarity and legal standing, especially in New York.

Individuals and businesses can also create promissory notes. They are not limited to financial institutions.

A valid promissory note must be signed by the borrower. The signature serves as an acknowledgment of the debt.

Interest rates can be either fixed or variable, depending on what the parties agree upon in the promissory note.

When properly executed, a promissory note is a legally binding contract. It obligates the borrower to repay the loan under the agreed terms.

While it is true that changes can complicate matters, amendments can be made if both parties agree and document the changes appropriately.

While not always required, having a witness or notarization can provide additional legal protection and help verify the agreement.

Promissory notes can be used for any amount, whether large or small. They are a flexible tool for personal and business loans.

Defaulting can lead to serious repercussions, including legal action and damage to credit scores. It is crucial to understand the implications before signing.

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money to a designated person or bearer at a future date or on demand. |

| Governing Law | The New York Uniform Commercial Code (UCC) governs promissory notes in New York. |

| Parties Involved | The note involves two primary parties: the maker (who promises to pay) and the payee (who receives the payment). |

| Interest Rate | The interest rate must be clearly stated. If not specified, the legal rate of interest applies. |

| Payment Terms | Payment terms should be clearly outlined, including the amount due and the due date. |

| Signatures | The maker's signature is required for the note to be valid. The payee's signature is not necessary. |

| Transferability | Promissory notes are generally negotiable instruments, meaning they can be transferred to others, subject to certain conditions. |

After obtaining the New York Promissory Note form, it is important to complete it accurately to ensure that all necessary information is included. This form serves as a written promise to repay a specified amount of money under agreed-upon terms. Follow the steps below to fill out the form correctly.