Blank Loan Agreement Template for the State of New York

Blank Loan Agreement Template for the State of New York

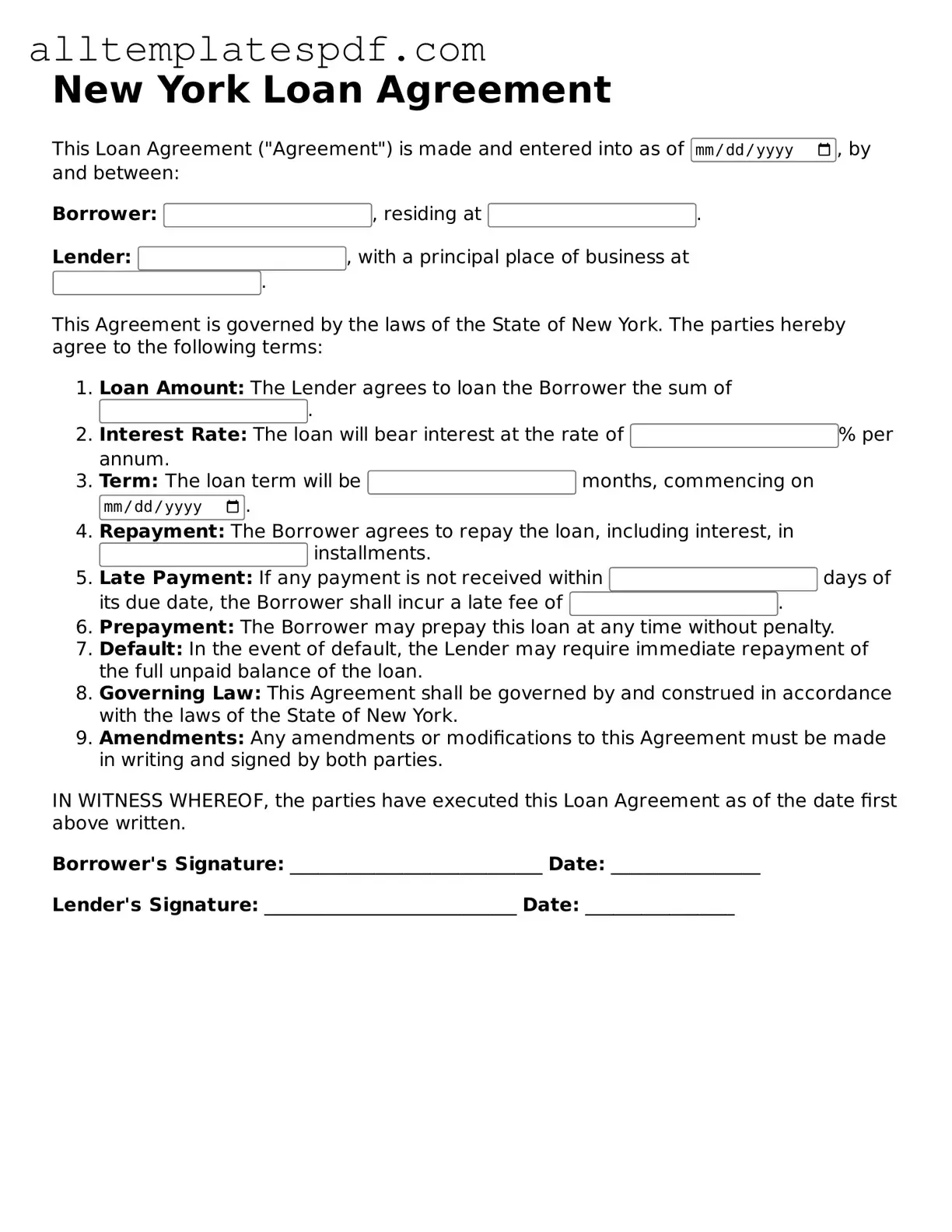

Completing a New York Loan Agreement form requires careful attention to detail. One common mistake is failing to provide accurate personal information. Borrowers often overlook the importance of entering their full legal name, current address, and Social Security number correctly. Inaccuracies can lead to delays in processing or even denial of the loan.

Another frequent error involves the loan amount. Individuals sometimes miscalculate the desired loan amount or neglect to specify it altogether. This omission can create confusion for lenders, as they need this information to assess the borrower's needs and eligibility.

In addition, many people forget to include the purpose of the loan. Lenders typically require this information to evaluate the risk associated with the loan. Without a clear explanation, the application may be deemed incomplete, leading to further complications.

Many borrowers also fail to read the terms and conditions thoroughly. Ignoring the fine print can result in misunderstandings about interest rates, repayment schedules, and fees. A lack of clarity on these terms can lead to financial strain later on.

Another mistake involves not providing the necessary documentation. Lenders often require proof of income, credit history, or other financial documents. Omitting these can delay the approval process or even result in rejection.

Some applicants neglect to sign the agreement. A missing signature renders the document invalid, which can lead to the entire application being dismissed. It is crucial to ensure that all required signatures are present before submission.

Additionally, individuals might overlook the importance of reviewing the completed form for errors. Typos or incorrect figures can compromise the integrity of the application. A thorough review can catch these mistakes before they cause issues.

Not disclosing existing debts is another pitfall. Lenders need a complete picture of the borrower's financial situation. Failing to disclose current obligations can lead to a lack of trust and potential rejection.

Finally, many borrowers underestimate the importance of following up after submission. A lack of communication can lead to uncertainty regarding the application status. Staying in touch with the lender can facilitate a smoother process and clarify any outstanding issues.

Free Promissory Note Template California - It may require the inclusion of a loan purpose to define how funds will be used.

When dealing with real estate transactions in New York, it's crucial to utilize the appropriate documentation, such as the New York Deed form, which can be conveniently obtained through resources like NY PDF Forms. This ensures that the transfer of ownership from the seller to the buyer is executed smoothly and legally.

Promissory Note Illinois - The agreement may address conditions for refinancing the loan.

Understanding the New York Loan Agreement form is crucial for anyone involved in borrowing or lending money. However, several misconceptions can lead to confusion. Below is a list of common misunderstandings about this important document.

Being aware of these misconceptions can help individuals navigate the complexities of the New York Loan Agreement form more effectively. Understanding the nuances can lead to better decision-making and a more secure borrowing experience.

| Fact Name | Description |

|---|---|

| Purpose | The New York Loan Agreement form is used to outline the terms of a loan between a lender and a borrower. |

| Governing Law | This agreement is governed by the laws of the State of New York. |

| Parties Involved | The form identifies the lender and borrower, including their legal names and contact information. |

| Loan Amount | The specific amount of money being borrowed is clearly stated in the agreement. |

| Interest Rate | The agreement specifies the interest rate applicable to the loan, whether fixed or variable. |

| Repayment Terms | Details about how and when the loan will be repaid are included, such as payment frequency and duration. |

| Default Clauses | The form outlines what constitutes a default and the consequences for the borrower in such cases. |

| Signatures | Both parties must sign the agreement to make it legally binding, indicating their acceptance of the terms. |

Completing the New York Loan Agreement form is a critical step in securing a loan. It requires attention to detail to ensure all necessary information is accurately provided. Follow these steps carefully to fill out the form correctly.

After completing the form, review it thoroughly to confirm all information is accurate. Keep a copy for your records, and provide the original to the other party involved in the agreement. This will ensure both parties have the necessary documentation for future reference.