Fill Out a Valid Mortgage Statement Form

Fill Out a Valid Mortgage Statement Form

Filling out a Mortgage Statement form can seem straightforward, but many individuals make common mistakes that can lead to confusion or even financial repercussions. Understanding these pitfalls can help ensure that your mortgage process goes smoothly.

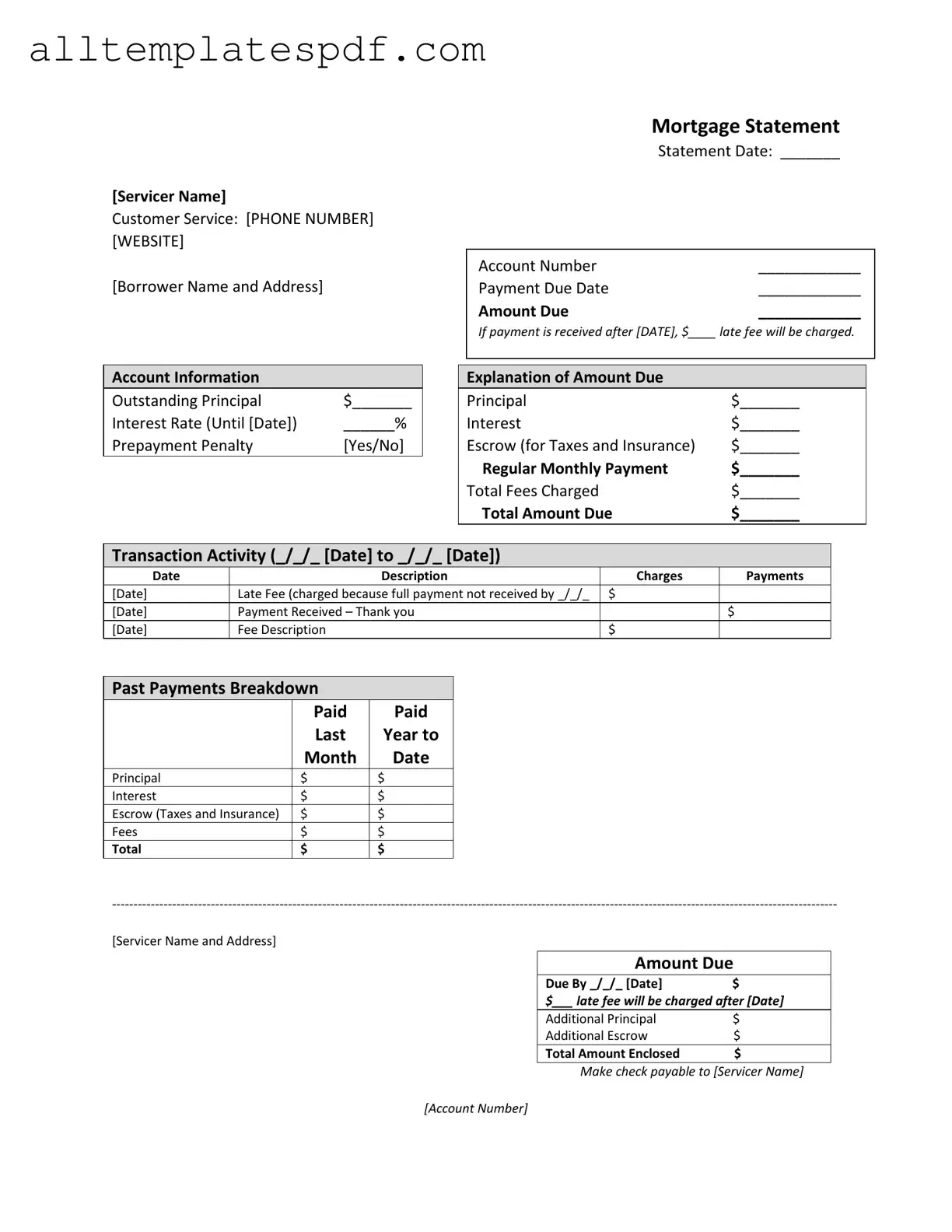

One frequent error occurs when borrowers fail to include their account number. This number is crucial for identifying your specific mortgage account. Without it, the servicer may struggle to process your payment or respond to your inquiries. Always double-check that you’ve entered the correct account number before submitting your form.

Another common mistake is neglecting to verify the payment due date. Many people assume they know when their payment is due, but it’s essential to confirm this date on the statement. Missing a payment deadline can lead to late fees and negatively impact your credit score.

Many individuals also overlook the section detailing the amount due. It’s important to ensure that you are sending the correct total. If you miscalculate or ignore additional fees, your payment may be insufficient, leading to further complications.

Additionally, some borrowers fail to read the important messages section carefully. This part often contains crucial information about partial payments and potential consequences of delinquency. Ignoring these messages can result in misunderstandings about your payment status and obligations.

Another mistake is not providing the correct contact information for the servicer. If you need assistance or have questions, having the right phone number and website is essential. Double-check that this information is accurate to avoid delays in communication.

Sometimes, individuals forget to include a check or payment method when submitting their forms. It’s easy to assume that the servicer will know you intend to pay, but without a payment included, your account may fall further behind.

People also often neglect to review their transaction history for accuracy. Ensure that all payments and charges are correctly listed. If there are discrepancies, address them promptly to avoid future issues.

Another frequent oversight involves ignoring the delinquency notice. This notice serves as a warning about the potential consequences of late payments. Being aware of your delinquency status can help you take action sooner rather than later.

Lastly, many borrowers fail to seek help when experiencing financial difficulty. The form often includes resources for mortgage counseling. If you find yourself struggling, reaching out for assistance can provide you with options and support to manage your mortgage effectively.

Home Load Calculation - It can also serve as a training document for those new to electrical design.

Completing the New York LS 665 form accurately is vital for PEOs to fulfill their regulatory obligations, and resources such as NY PDF Forms can provide valuable guidance during the application process, ensuring that all necessary information is submitted correctly to avoid any registration issues.

Faa 8050-2 - The Aircraft Bill of Sale is accepted by the Federal Aviation Administration.

There are several misconceptions regarding the Mortgage Statement form that can lead to confusion among borrowers. Below are five common misconceptions explained.

In reality, the Mortgage Statement may not reflect every payment made. It typically shows the current status, including any unpaid balances, but may not include details of every transaction.

While the statement indicates a late fee will apply if payment is not received by a certain date, it is essential to understand that fees are only charged if the payment is indeed late. Timely payments will not incur any additional fees.

This is incorrect. According to the statement, partial payments are held in a suspense account and do not reduce the mortgage balance until the full payment is made. Borrowers should ensure they pay the full amount due to avoid complications.

The Mortgage Statement may indicate that the interest rate is valid only until a specified date. After that date, the interest rate could change, affecting future payments. Borrowers should be aware of when their interest rate may adjust.

The statement includes a summary of recent account history but may not provide a comprehensive view of all past payments. Borrowers looking for detailed transaction history should request additional documentation from their servicer.

| Fact Name | Description |

|---|---|

| Servicer Information | The mortgage statement includes the servicer's name, customer service phone number, and website for easy contact. |

| Borrower Details | It lists the borrower's name and address, ensuring that all information is personalized. |

| Statement Date | The statement date indicates when the information was prepared, helping borrowers track their payments. |

| Payment Due Date | This date shows when the next payment is due, which is crucial for avoiding late fees. |

| Late Fees | If payment is not received by the specified date, a late fee will be charged, which is clearly stated. |

| Outstanding Principal | The statement provides the outstanding principal amount, allowing borrowers to see how much they owe. |

| Interest Rate | The current interest rate is listed, along with the date it is valid until, giving borrowers clarity on their loan terms. |

| Prepayment Penalty | Information on whether there is a prepayment penalty is included, helping borrowers understand potential costs. |

| Transaction Activity | A section details recent transactions, including payments and any late fees charged, providing a clear account history. |

| Financial Assistance | The statement offers information on mortgage counseling for borrowers experiencing financial difficulties. |

Filling out the Mortgage Statement form requires attention to detail to ensure all necessary information is accurately recorded. After completing the form, it is important to review it for any errors before submission.

Once the form is filled out, review it carefully to ensure all information is accurate and complete. This will help avoid any potential issues with your mortgage account.