Fill Out a Valid IRS 1120 Form

Fill Out a Valid IRS 1120 Form

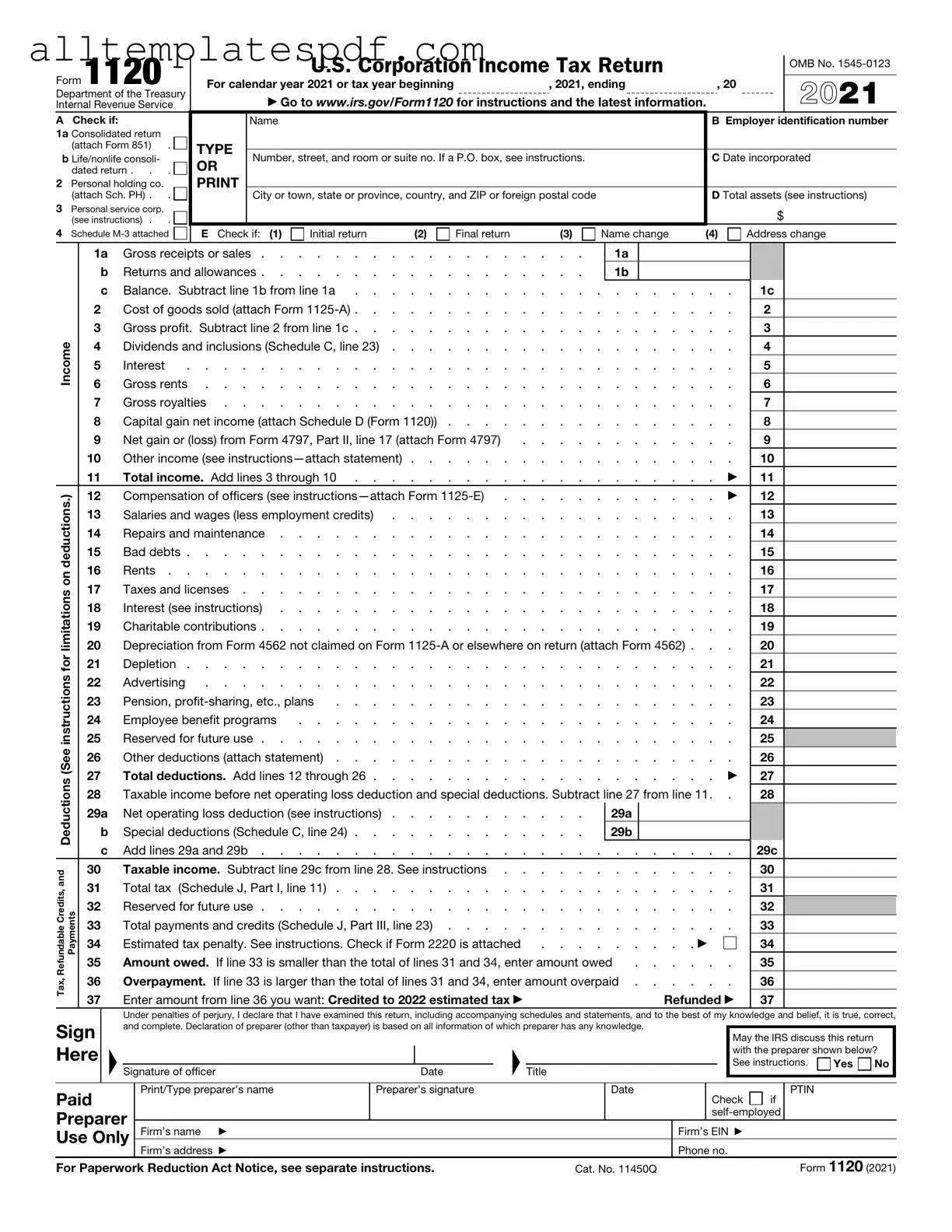

Filling out the IRS Form 1120, which is used by corporations to report their income, can be a complex task. Many individuals and businesses make common mistakes that can lead to delays, penalties, or even audits. Understanding these pitfalls is crucial for ensuring compliance and avoiding unnecessary complications.

One frequent mistake is failing to report all income. Corporations must include all sources of income, including sales, interest, and dividends. Omitting any income can raise red flags with the IRS, potentially leading to penalties. It’s essential to keep thorough records and ensure that every dollar earned is reported accurately.

Another common error is incorrectly calculating deductions. Corporations can deduct a variety of business expenses, but these must be legitimate and properly documented. Many people mistakenly claim expenses that are not deductible or miscalculate the amounts. This not only affects the tax liability but can also lead to audits if the IRS questions the legitimacy of these deductions.

Many filers also overlook the importance of signing the form. It may seem trivial, but an unsigned Form 1120 is considered incomplete. This oversight can delay processing and result in penalties. Always double-check to ensure that all required signatures are present before submission.

Another mistake involves using the wrong tax year. Corporations must ensure they are filing for the correct tax year. Filing for the wrong year can lead to confusion and potential issues with the IRS. It’s important to verify the tax year before completing the form.

Moreover, neglecting to include all necessary schedules can be detrimental. Depending on the corporation's activities, additional schedules may be required to provide a complete picture of the financial situation. Failing to include these can lead to incomplete filings and further inquiries from the IRS.

In addition, not keeping up with changes in tax laws can lead to errors. Tax laws frequently change, and it’s vital to stay informed about any updates that may affect how the Form 1120 should be filled out. Relying on outdated information can result in mistakes that could have been easily avoided.

Finally, many people underestimate the importance of reviewing the form before submission. A thorough review can catch simple mistakes, such as typos or miscalculations, that could have significant consequences. Taking the time to carefully examine the completed form can save a lot of trouble down the line.

Odometer Statement Indiana - This statement helps protect buyers from potential fraud related to odometer tampering.

Western Union Receipt Generator - Transfer funds quickly and securely to friends or family.

For couples preparing for marriage, understanding the significance of a well-drafted prenuptial agreement template can be invaluable in establishing clear terms for asset division should the need arise. This document serves as a foundation for open communication regarding financial matters, ultimately fostering trust between partners.

Signed Real Doctors Note for Work - Includes necessary details without overwhelming the reader.

The IRS Form 1120 is an essential document for corporations, but several misconceptions surround it. Understanding these can help ensure compliance and avoid unnecessary complications. Here are four common misconceptions about the IRS Form 1120:

Understanding these misconceptions can help corporations navigate their tax obligations more effectively. Proper filing ensures compliance and can prevent potential penalties or issues with the IRS.

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 1120 is used by corporations to report their income, gains, losses, deductions, and credits. |

| Filing Requirement | Corporations must file Form 1120 annually, regardless of whether they owe taxes. |

| Due Date | The due date for filing Form 1120 is the 15th day of the fourth month after the end of the corporation's tax year. |

| Estimated Taxes | Corporations may need to make estimated tax payments if they expect to owe tax of $500 or more. |

| Tax Rate | The corporate tax rate is a flat 21% as of 2023, following the Tax Cuts and Jobs Act. |

| State-Specific Forms | Many states require their own corporate tax forms, such as Form 1120-S in California, governed by California Revenue and Taxation Code. |

| Filing Methods | Form 1120 can be filed electronically or by mail, depending on the corporation's preference. |

| Supporting Documents | Corporations must attach supporting schedules and documents, such as balance sheets and income statements. |

| Penalties | Late filing can result in penalties, which may include a fine based on the number of months the return is late. |

| Amended Returns | If a corporation needs to correct a filed Form 1120, it must submit Form 1120-X to amend the return. |

Filling out the IRS Form 1120 is an essential task for corporations to report their income, gains, losses, deductions, and credits. Completing this form accurately is crucial for compliance with federal tax regulations. Below are the steps to guide you through the process of filling out the form.