Blank Promissory Note Template for the State of Illinois

Blank Promissory Note Template for the State of Illinois

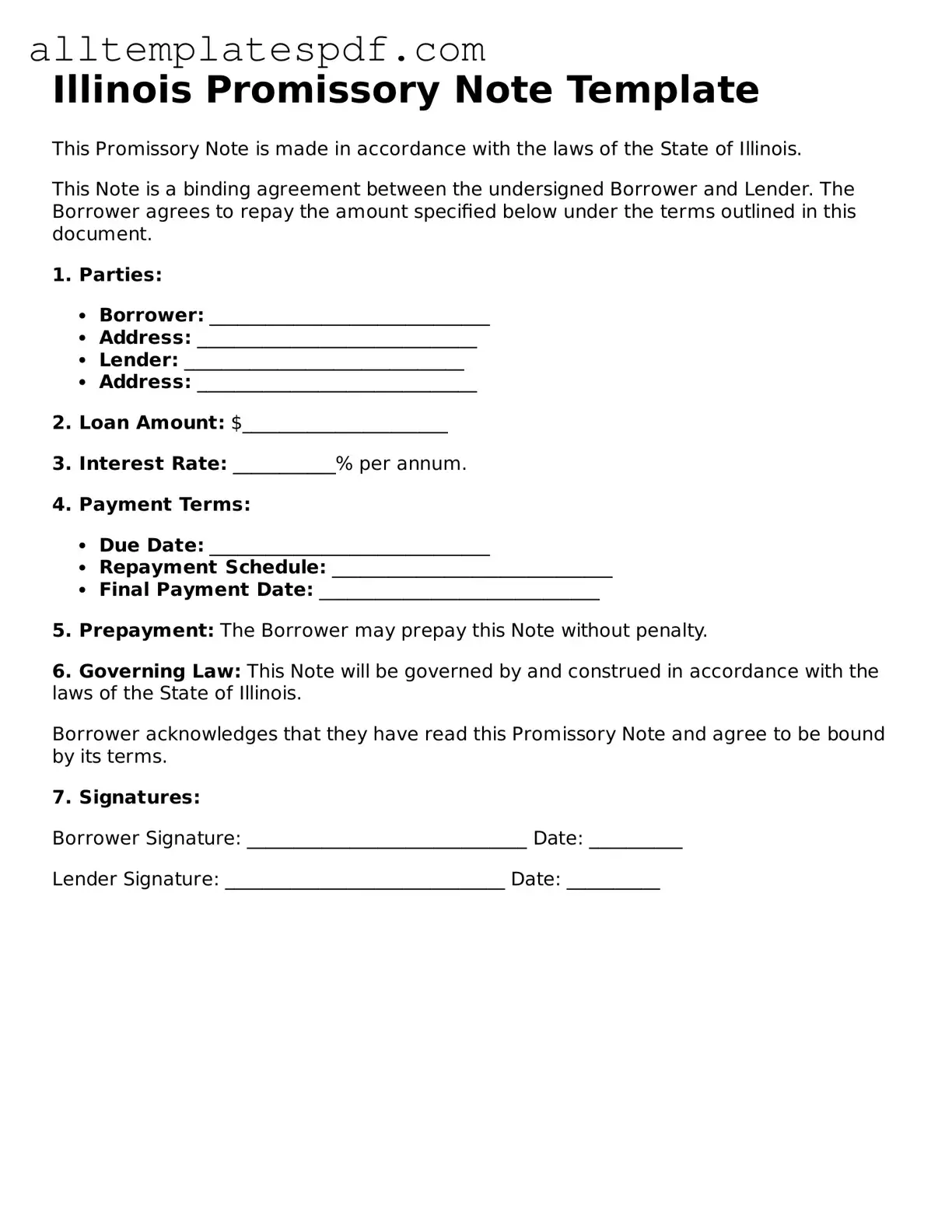

Filling out the Illinois Promissory Note form can seem straightforward, but there are common mistakes that individuals often make. One frequent error is not including all necessary information. The form requires specific details such as the names and addresses of both the borrower and the lender. Omitting any of this information can lead to confusion or disputes later on.

Another mistake is failing to specify the loan amount clearly. The amount should be written both in numbers and in words to avoid any ambiguity. If the two amounts do not match, it may cause complications when enforcing the note. Clarity is crucial in financial agreements.

People also sometimes neglect to include the interest rate. If the loan is to accrue interest, it’s essential to state the rate explicitly. Without this information, the terms of repayment can become unclear, leading to misunderstandings between the parties involved.

Additionally, some individuals forget to include the repayment schedule. Whether the borrower will make monthly payments or a lump sum at the end should be clearly outlined. This schedule helps both parties understand their obligations and can prevent missed payments.

Finally, many overlook the importance of signatures. Both the borrower and the lender must sign the document for it to be legally binding. Failing to do so can render the note invalid, which defeats its purpose. Taking the time to ensure that all signatures are present can save significant trouble in the future.

Online Promissory Note - The borrower’s creditworthiness often influences the terms provided.

Simple Promissory Note Template California - A promissory note can facilitate trust between a borrower and lender through clear terms.

Promissory Note Template Ohio - Promissory notes may also include a provision for attorney's fees in case of collection disputes.

To facilitate the process of finalizing a divorce, parties should consider using a New York Divorce Settlement Agreement form, which can greatly clarify the terms of their separation. For those looking for a structured template, the NY PDF Forms is an excellent resource to ensure all necessary details are included for a smooth transition into the next chapter of their lives.

Promissory Note Template Georgia - If disputes arise, the promissory note can be used in court to demonstrate the agreement made.

Understanding the Illinois Promissory Note form can be tricky, especially with the many misconceptions that exist. Here are seven common misunderstandings about this important financial document:

Many people believe that a promissory note is a one-size-fits-all document. In reality, each note can vary significantly based on the terms, parties involved, and state laws. The Illinois Promissory Note form has specific requirements that must be met to be valid in the state.

Some think that a verbal promise to pay is enough. However, while verbal agreements can be legally binding, having a written promissory note is crucial. It provides clear evidence of the terms and can help avoid disputes.

This is a common myth. Individuals and businesses can create promissory notes, not just financial institutions. Anyone lending money can use this form to formalize the agreement.

Many believe that promissory notes are only necessary for significant amounts of money. However, they can be used for any loan amount, big or small. Having a formal document is always a good practice.

Some think that once a promissory note is executed, it is set in stone. In fact, parties can amend the note if both agree to the changes. It’s essential to document any modifications properly.

While notarization is not always required, having a promissory note notarized can add an extra layer of legitimacy. It helps verify the identities of the parties involved and can be beneficial if disputes arise.

This misconception can lead to serious financial trouble. Defaulting on a promissory note can result in legal action, damage to credit scores, and additional financial penalties. It’s crucial to understand the responsibilities that come with signing.

By dispelling these misconceptions, individuals can better navigate the complexities of promissory notes in Illinois and make informed decisions about their financial agreements.

| Fact Name | Description |

|---|---|

| Definition | An Illinois Promissory Note is a written promise to pay a specified amount of money to a designated person or entity at a specified time. |

| Governing Law | The Illinois Uniform Commercial Code (UCC) governs promissory notes in Illinois. |

| Parties Involved | The document typically involves two parties: the maker (who promises to pay) and the payee (who receives the payment). |

| Interest Rate | The interest rate can be specified in the note. If not, the legal rate of interest in Illinois applies. |

| Payment Terms | Payment terms must be clearly stated, including the due date and any installment arrangements. |

| Signature Requirement | The note must be signed by the maker to be legally binding. A digital signature may be acceptable under certain conditions. |

| Default Consequences | In case of default, the payee has the right to pursue legal action to recover the owed amount, including interest and fees. |

| Transferability | Promissory notes can be transferred or assigned to another party unless explicitly stated otherwise in the document. |

| Notarization | While notarization is not required, it can provide additional legal protection and verification of the parties' identities. |

After you have gathered all necessary information, you are ready to fill out the Illinois Promissory Note form. This process involves entering specific details accurately to ensure that the document serves its intended purpose. Follow the steps below to complete the form correctly.

After completing the form, ensure that both parties keep a copy for their records. This document is now ready to be executed and should be stored safely to avoid any disputes in the future.