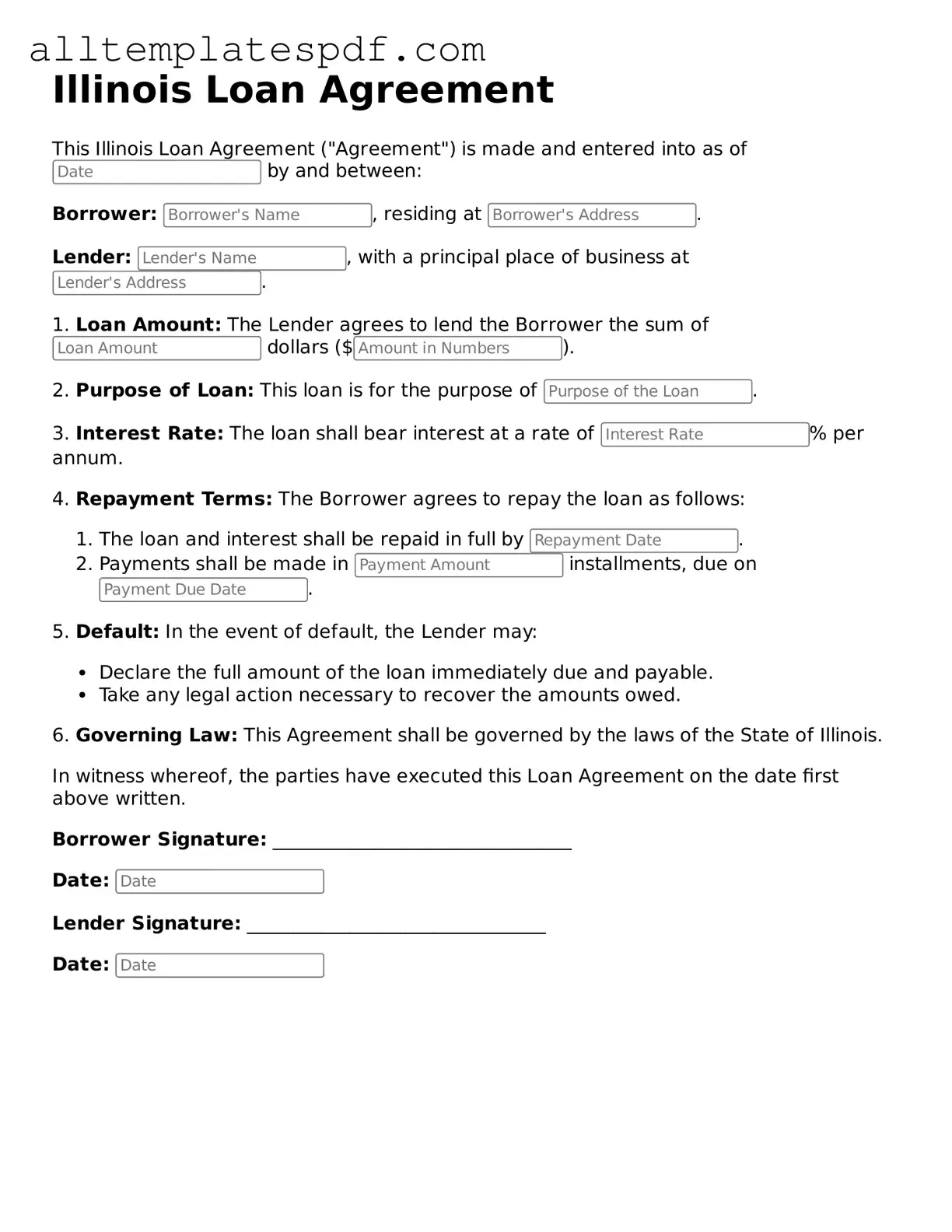

Blank Loan Agreement Template for the State of Illinois

Blank Loan Agreement Template for the State of Illinois

Filling out the Illinois Loan Agreement form can seem straightforward, but many people make common mistakes that can lead to confusion or even legal issues down the line. One frequent error is not providing accurate personal information. This includes your name, address, and contact details. If any of this information is incorrect, it can complicate matters if you need to communicate with the lender or if there are disputes later on.

Another mistake involves overlooking the loan amount. Some individuals either write down the wrong figure or fail to include any additional fees associated with the loan. It's crucial to ensure that the total amount accurately reflects what you are borrowing. If discrepancies arise, it may lead to misunderstandings about repayment terms.

People often forget to read the terms and conditions thoroughly. Skimming through this section can result in missing important details about interest rates, repayment schedules, and penalties for late payments. Understanding these terms is essential to avoid surprises later. A clear grasp of the agreement helps in managing expectations and responsibilities.

In addition, many borrowers neglect to sign and date the form. Without a signature, the agreement is not legally binding. This simple oversight can invalidate the entire document, leaving both parties in a precarious situation. Always double-check that you have signed and dated the agreement before submission.

Another common error is failing to provide the necessary documentation. Lenders often require supporting documents such as proof of income or identification. If these documents are missing, it can delay the loan process or even result in denial of the application. Ensure you have all required paperwork ready to avoid setbacks.

Some individuals also misinterpret the repayment terms. They might assume that the repayment period is longer or shorter than it actually is. This misunderstanding can lead to financial strain if borrowers expect more time to repay than what is stipulated in the agreement. Clarifying these terms before signing is vital.

Lastly, many people do not keep a copy of the signed agreement. After all, it’s essential to have a record of what was agreed upon. Without a copy, you may find it challenging to refer back to the terms if questions or issues arise. Always request a copy for your records, ensuring you have documentation of the agreement.

Free Promissory Note Template Texas - Includes sections for borrower signatures and dates.

Florida Promissory Note - Many lenders require a loan agreement before disbursing any funds.

When navigating the complexities of divorce, utilizing a comprehensive resource can make the process smoother. By employing a New York Divorce Settlement Agreement form, individuals can ensure that all crucial terms are clearly articulated. This document addresses vital considerations such as asset division, debt responsibilities, child custody, and spousal support. For those seeking a convenient template, NY PDF Forms provides an excellent starting point to create a well-structured agreement that protects the interests of both parties.

Promissory Note Template Georgia - Offers clarity on the interest charged for the borrowed amount.

Understanding the Illinois Loan Agreement form can be challenging, especially with various misconceptions floating around. Here are eight common myths and the truths that dispel them.

This is not true. The form can be used for loans of any size, whether small personal loans or larger business loans. It provides a structured way to outline the terms regardless of the amount.

While having legal advice can be beneficial, it is not strictly necessary. Many individuals successfully complete the form on their own by carefully following the instructions and understanding the terms involved.

In reality, anyone lending money—friends, family, or acquaintances—should consider using the form. It helps clarify expectations and protects both parties.

Loan terms can be modified, but both parties must agree to any changes. It’s essential to document any amendments in writing to avoid confusion later on.

While both documents relate to loans, they serve different purposes. The loan agreement outlines the terms and conditions, while a promissory note is a promise to repay the loan.

Even in personal loans, interest rates can be important. They impact the total amount that will be repaid, so it’s wise to clarify this in the agreement.

The Illinois Loan Agreement form is designed for written agreements, but it can also serve as a reference for verbal agreements. However, having a written document is always the best practice.

While the form is versatile, it may not be suitable for every type of loan, such as those secured by real estate. Always ensure that the form aligns with the specific type of loan you are dealing with.

By debunking these misconceptions, borrowers and lenders can approach the Illinois Loan Agreement form with greater confidence and clarity.

| Fact Name | Description |

|---|---|

| Purpose | The Illinois Loan Agreement form is used to outline the terms and conditions of a loan between a lender and a borrower. |

| Governing Law | This agreement is governed by the laws of the State of Illinois. |

| Parties Involved | The form requires the names and addresses of both the lender and the borrower. |

| Loan Amount | The specific amount of money being loaned must be clearly stated in the agreement. |

| Interest Rate | The interest rate applicable to the loan should be included, whether fixed or variable. |

| Repayment Terms | Details about repayment schedules, including due dates and payment methods, are essential. |

| Default Terms | The agreement outlines what constitutes a default and the consequences of defaulting on the loan. |

| Signatures | Both parties must sign the agreement to make it legally binding. |

Completing the Illinois Loan Agreement form is an important step in securing a loan. By following these steps carefully, you will ensure that all necessary information is provided accurately. This will help both parties understand their rights and responsibilities in the loan arrangement.