Fill Out a Valid Gift Letter Form

Fill Out a Valid Gift Letter Form

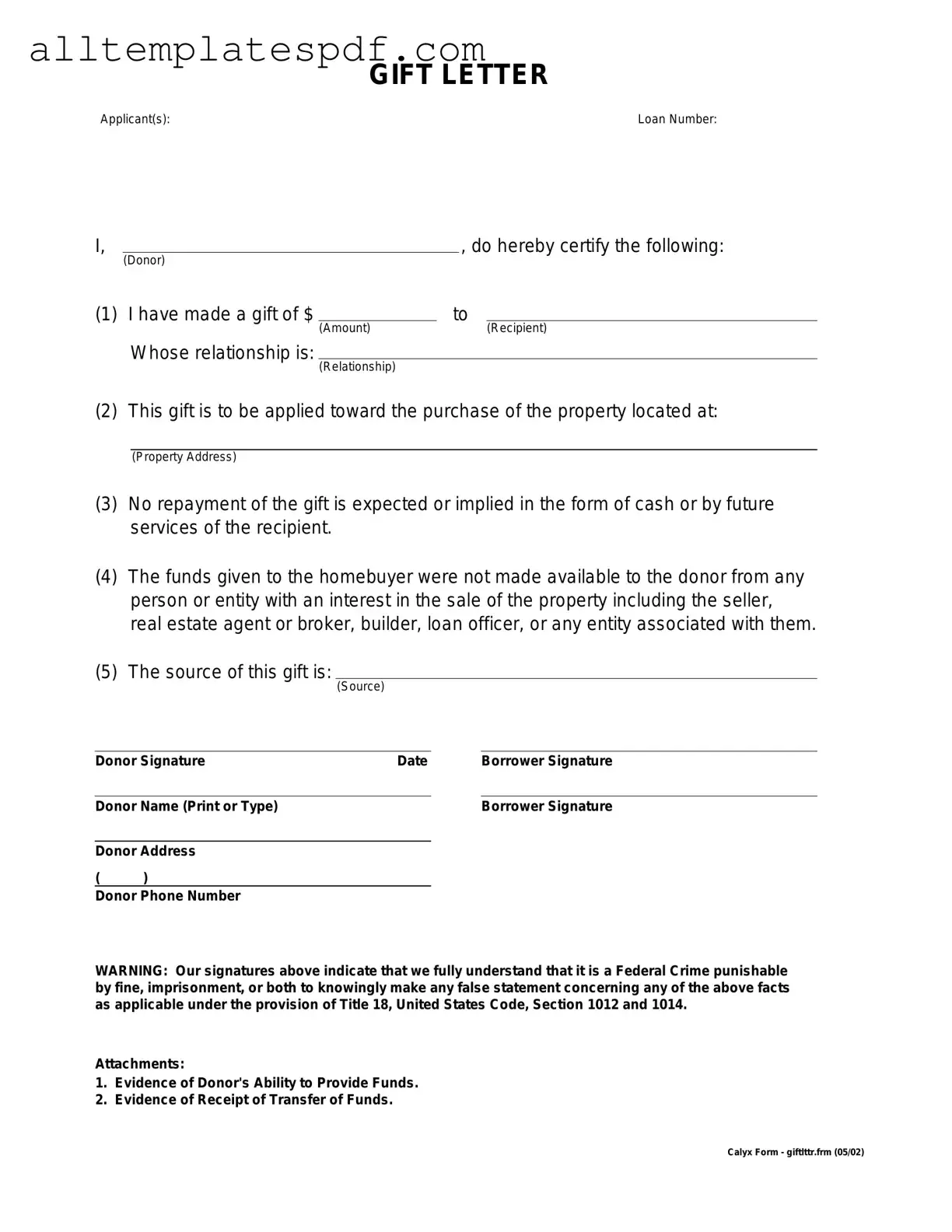

Filling out a Gift Letter form can seem straightforward, but many people make common mistakes that can lead to delays or complications. One frequent error is not including all required information. Each section of the form must be completed accurately. Omitting details such as the donor's address or the recipient's relationship to the donor can raise red flags for lenders.

Another mistake is failing to provide a clear statement about the nature of the gift. The form should explicitly state that the funds are a gift and not a loan. If the language is ambiguous, it could cause confusion or lead to scrutiny from financial institutions.

Many individuals also neglect to sign the Gift Letter. A signature is crucial, as it signifies the donor's intention to give the funds without expecting repayment. Without this, the letter may be deemed invalid, jeopardizing the transaction.

Inaccurate dates are another common pitfall. The date of the gift should reflect when the funds were transferred or are intended to be transferred. Incorrect or inconsistent dates can create doubts about the legitimacy of the gift.

People often forget to include the source of the funds. Lenders may require an explanation of where the gift money originated. Providing this information helps to establish the legitimacy of the gift and can facilitate the approval process.

Additionally, some individuals mistakenly use vague language. Instead of stating the exact amount of the gift, they may write "approximately" or "around." This lack of specificity can lead to complications, as lenders prefer clear and precise information.

Finally, failing to consult with a professional can be a critical error. Many people overlook the importance of having their Gift Letter reviewed by a lawyer or financial advisor. This oversight can result in missed opportunities for clarity and compliance with legal standards.

Da - The form features a section for listing the condition codes of the items.

The important Notary Acknowledgement form is necessary for properly executing various documents and ensuring that all signatures are validated by a qualified notary public, thereby enhancing the legality of transactions.

Melaleuca Cancelation Form - Upon cancellation, customers lose benefits like discounts and Loyalty Shopping Dollars.

P45 Form - Tax codes play a significant role and should be filled out carefully to avoid complications.

Understanding the Gift Letter form is crucial for anyone involved in real estate transactions, especially first-time homebuyers. However, several misconceptions can lead to confusion. Here are five common misunderstandings:

This is not true. While first-time homebuyers often use gift letters to show that they received funds from family or friends, anyone receiving a monetary gift for a home purchase can use this form.

A gift letter does not guarantee that a loan will be approved. It simply provides documentation that the funds are a gift and not a loan, which is an important distinction for lenders.

This is a misconception. While family members are the most common sources of gifts, friends and other individuals can also provide financial assistance. However, lenders may have specific requirements about who qualifies as a donor.

Notarization is not a requirement for gift letters in most cases. However, some lenders may request notarized letters for added verification, so it is essential to check with the lender's specific requirements.

This is misleading. Even small gifts can require a gift letter if they are used to cover part of the down payment. Lenders want to ensure that all funds are accounted for, regardless of the amount.

Clearing up these misconceptions can help individuals navigate the home-buying process more effectively. Always consult with a lender or real estate professional for guidance tailored to your situation.

| Fact Name | Description |

|---|---|

| Purpose of Gift Letter | A gift letter is used to document a financial gift, typically from a family member, to assist in purchasing a home. It confirms that the funds do not need to be repaid. |

| Required Information | The letter must include the donor's name, address, relationship to the recipient, the amount of the gift, and a statement that the funds are a gift, not a loan. |

| State-Specific Requirements | Some states may have specific requirements for gift letters. For instance, California requires a signed statement from the donor indicating the gift's purpose and amount, per California Civil Code Section 1624. |

| Impact on Mortgage Approval | Lenders often require a gift letter as part of the mortgage application process. This document helps ensure that the borrower meets the necessary financial criteria without incurring additional debt. |

Once you have the Gift Letter form in front of you, it’s time to fill it out accurately. This form is essential for documenting the financial support you are receiving. Follow the steps below to ensure you complete it correctly.

After completing these steps, the form is ready to be submitted as part of your financial documentation. Ensure that all details are correct to avoid any issues down the line.