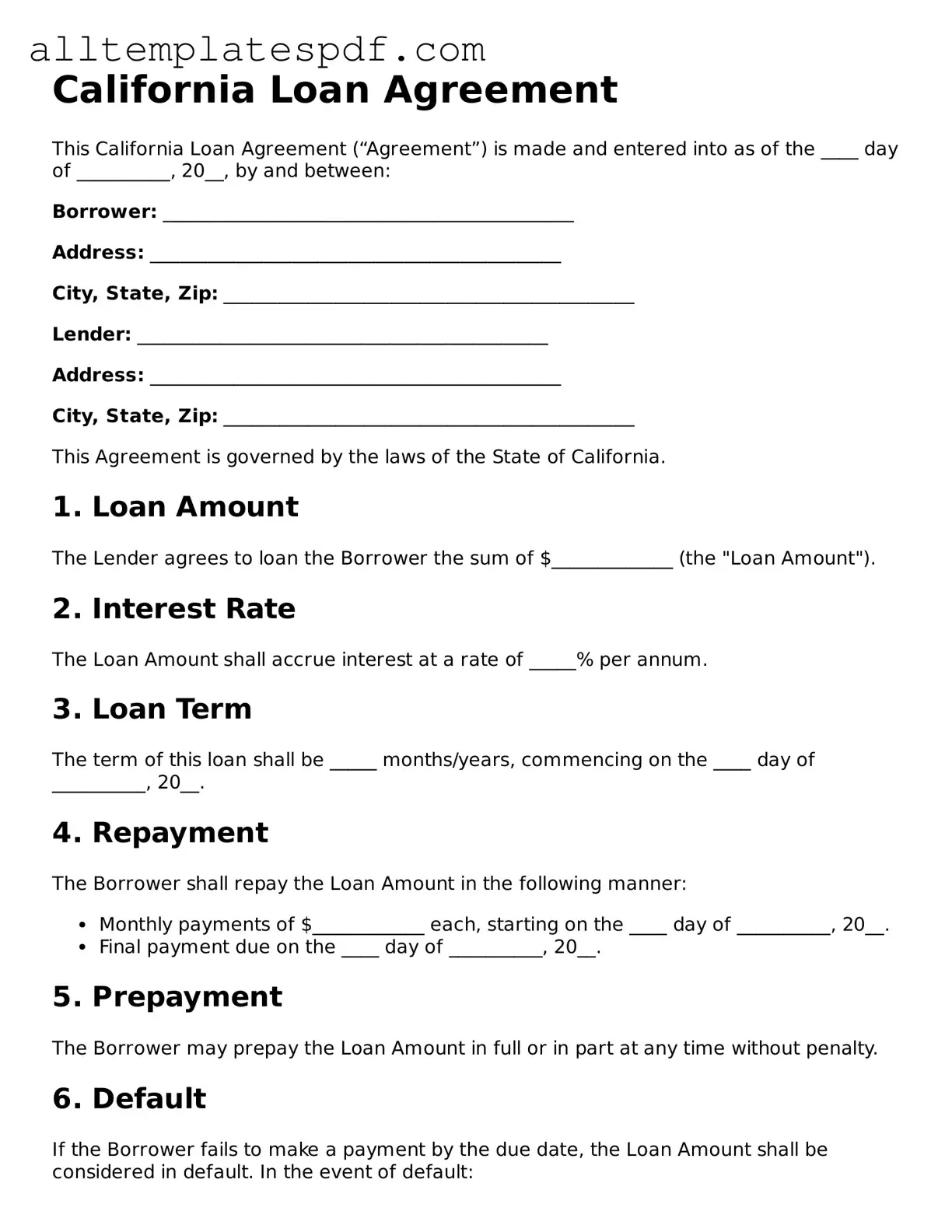

Blank Loan Agreement Template for the State of California

Blank Loan Agreement Template for the State of California

Filling out the California Loan Agreement form can be a straightforward process, but several common mistakes can lead to complications. One frequent error is failing to provide complete and accurate borrower information. This includes not only the name but also the correct address and contact details. Incomplete information can delay the processing of the loan and create issues in communication.

Another common mistake is neglecting to specify the loan amount clearly. Borrowers often either write an incorrect figure or omit the amount altogether. This oversight can lead to misunderstandings about the terms of the loan and may result in disputes later on. It’s crucial to ensure that the loan amount is clearly stated and matches the agreed-upon figure.

Additionally, many individuals overlook the importance of detailing the repayment terms. This includes the interest rate, payment schedule, and any late fees. Without these specifics, both parties may have different expectations about how and when the loan will be repaid. Clarity in these terms is essential to avoid future conflicts.

Moreover, some borrowers fail to sign and date the agreement. An unsigned document may not hold up legally, leaving the lender without recourse if issues arise. It is vital to ensure that all necessary signatures are present and that the date reflects when the agreement was finalized.

Lastly, individuals often do not read the entire agreement before signing. Skimming through the document can lead to missing important clauses or conditions that could affect the loan. Taking the time to thoroughly review the agreement helps ensure that all parties are on the same page and reduces the likelihood of disputes down the line.

Florida Promissory Note - It establishes clear terms around the loan’s purpose and use of funds.

The New York 810 form is an official document used typically by law enforcement agencies to report certain types of incidents. It's a critical component of the administrative process that ensures incidents are recorded accurately and consistently. This form not only facilitates a streamlined approach for documentation but also serves as a vital record for future reference and accountability, which can be further understood through resources like NY PDF Forms.

Free Promissory Note Template Texas - Includes identification of the loan type: secured or unsecured.

Promissory Note Template Georgia - Functions as an enforceable contract upon signature.

Promissory Note Illinois - It may outline state laws governing the loan terms.

Understanding the California Loan Agreement form can be challenging. Here are ten common misconceptions about this form, along with clarifications.

Loan agreements can vary significantly based on the type of loan, the lender's policies, and the borrower's needs. The California Loan Agreement form is tailored to comply with state laws and specific requirements.

While banks are common lenders, many other entities, including credit unions and private lenders, can provide loans. The California Loan Agreement can be used with various types of lenders.

Loan agreements, including the California Loan Agreement, are legally binding contracts. Both parties must adhere to the terms outlined in the agreement.

Loan agreements can be modified if both parties agree to the changes. However, any modifications should be documented in writing to maintain clarity.

Both the lender and the borrower must sign the California Loan Agreement for it to be valid. This ensures that both parties acknowledge and accept the terms.

Interest rates can be either fixed or variable, depending on the terms agreed upon in the California Loan Agreement. Borrowers should review these details carefully.

Loan agreements can be used for various amounts, not just large loans. They are applicable for personal loans, business loans, and more, regardless of the sum.

While some loans are secured by collateral, others may be unsecured. The California Loan Agreement form can accommodate both types of loans.

While the form itself may be straightforward, the loan approval process can take time. Factors such as credit checks and documentation can affect the timeline.

While it is not mandatory, seeking legal advice can be beneficial. Understanding the terms and implications of a loan agreement can help borrowers make informed decisions.

| Fact Name | Description |

|---|---|

| Governing Law | The California Loan Agreement is governed by the California Civil Code. |

| Parties Involved | The agreement typically involves a lender and a borrower, both of whom must be identified. |

| Loan Amount | The specific amount of money being loaned must be clearly stated in the agreement. |

| Interest Rate | The agreement must specify the interest rate applicable to the loan, which cannot exceed state limits. |

| Repayment Terms | Clear repayment terms, including the schedule and method of payment, should be outlined. |

| Default Conditions | The agreement should define what constitutes a default and the consequences thereof. |

| Signatures Required | Both parties must sign the agreement for it to be legally binding. |

Completing the California Loan Agreement form is a crucial step in establishing the terms of a loan between parties. It is essential to ensure that all information is accurate and clearly stated. Following these steps will help you fill out the form correctly.

After completing the form, it is advisable to keep copies for both the lender and the borrower. This ensures that both parties have a record of the agreement and its terms.