Fill Out a Valid Business Credit Application Form

Fill Out a Valid Business Credit Application Form

Filling out a Business Credit Application form can be a daunting task, and many people inadvertently make mistakes that can hinder their chances of approval. One common error is providing incomplete information. When applicants leave out crucial details, such as business address or contact information, it raises red flags for lenders. They need a complete picture to assess the creditworthiness of a business.

Another frequent mistake involves inaccuracies in financial data. Misstating income or expenses can lead to a denial of credit. It's essential to provide precise figures. Double-checking these numbers ensures that they reflect the true financial state of the business.

Many applicants also fail to review their credit history before applying. Not knowing their credit score or having unresolved issues can result in unexpected denials. Understanding one’s credit profile allows for proactive measures to improve it before submitting an application.

In addition, some people neglect to read the fine print. The terms and conditions of the credit agreement often contain important information regarding interest rates and fees. Ignoring these details can lead to unpleasant surprises later on.

Another mistake is not tailoring the application to the specific lender. Each lender may have unique requirements or preferences. Customizing the application to align with these expectations can significantly enhance the chances of approval.

Providing outdated or irrelevant documentation is also a common pitfall. Lenders require current financial statements and tax returns. Submitting old documents can signal disorganization and may lead to delays or rejections.

Lastly, some applicants rush through the process. Taking the time to carefully fill out the application and ensuring all sections are completed can make a significant difference. A thorough approach reflects professionalism and attention to detail, qualities that lenders appreciate.

96 Well Plate Diameter - Through its design, it allows for effective sample management in larger studies.

Affidavit of Support - The I-864 must be submitted by anyone sponsoring a relative for a visa.

Employer's Quarterly Federal Tax Return - Form 941 requires the employer identification number (EIN) for accurate processing.

When it comes to the Business Credit Application form, several misconceptions can lead to confusion. Understanding these misconceptions can help you navigate the application process more smoothly.

This is not true. Small businesses and startups can also apply for credit. The form is designed for any business seeking to establish or improve its credit profile.

Submitting the application does not guarantee that your business will receive credit. Lenders will evaluate various factors, including credit history and financial stability, before making a decision.

In many cases, lenders will consider the owner's personal credit score, especially for new businesses. A strong personal credit history can positively influence the outcome of the application.

Each lender may have different requirements and criteria. It’s important to review the specific guidelines of each lender to ensure you meet their expectations.

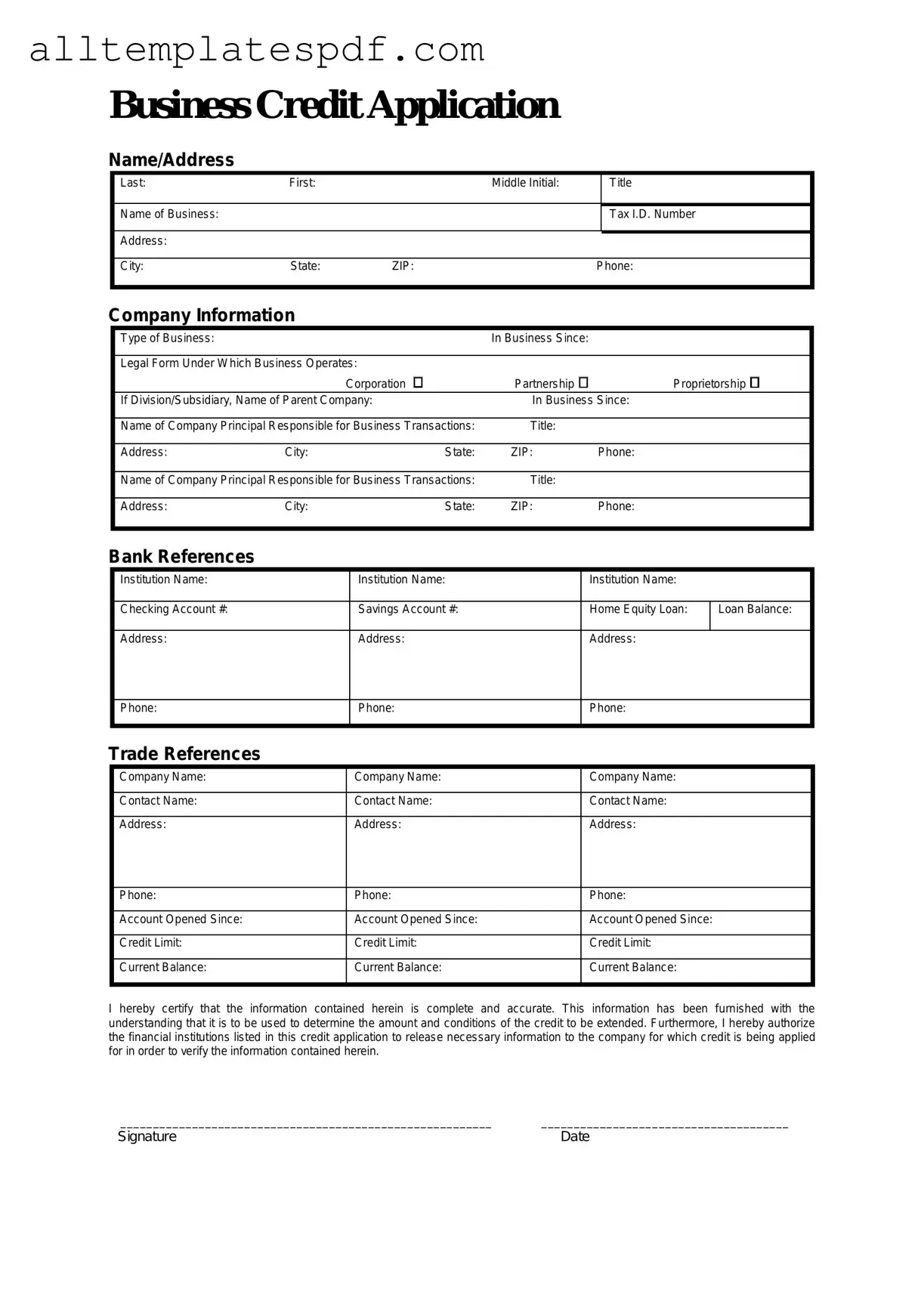

| Fact Name | Description |

|---|---|

| Purpose | The Business Credit Application form is used by businesses to apply for credit from suppliers or lenders. |

| Information Required | This form typically requires details about the business, including its legal name, address, and contact information. |

| Ownership Details | Applicants must provide information about the business owners, including their names and social security numbers. |

| Financial Information | Businesses often need to disclose financial statements or bank references to demonstrate creditworthiness. |

| State-Specific Forms | Some states may have specific forms that comply with local regulations; check state laws for details. |

| Governing Laws | In California, for example, the California Commercial Code governs credit applications. |

| Signature Requirement | The form usually requires a signature from an authorized representative of the business, confirming the accuracy of the information. |

| Submission Process | Completed forms can be submitted online or in person, depending on the creditor's requirements. |

| Review Timeline | After submission, the review process can take anywhere from a few days to a few weeks, depending on the lender's policies. |

Once you have the Business Credit Application form in front of you, the next steps involve carefully filling it out to ensure that all necessary information is provided. Accuracy is crucial, as this information will help facilitate the credit evaluation process.

After completing the form, submit it to the appropriate department as instructed. Ensure that you keep a copy for your records, as this may be useful for future reference.